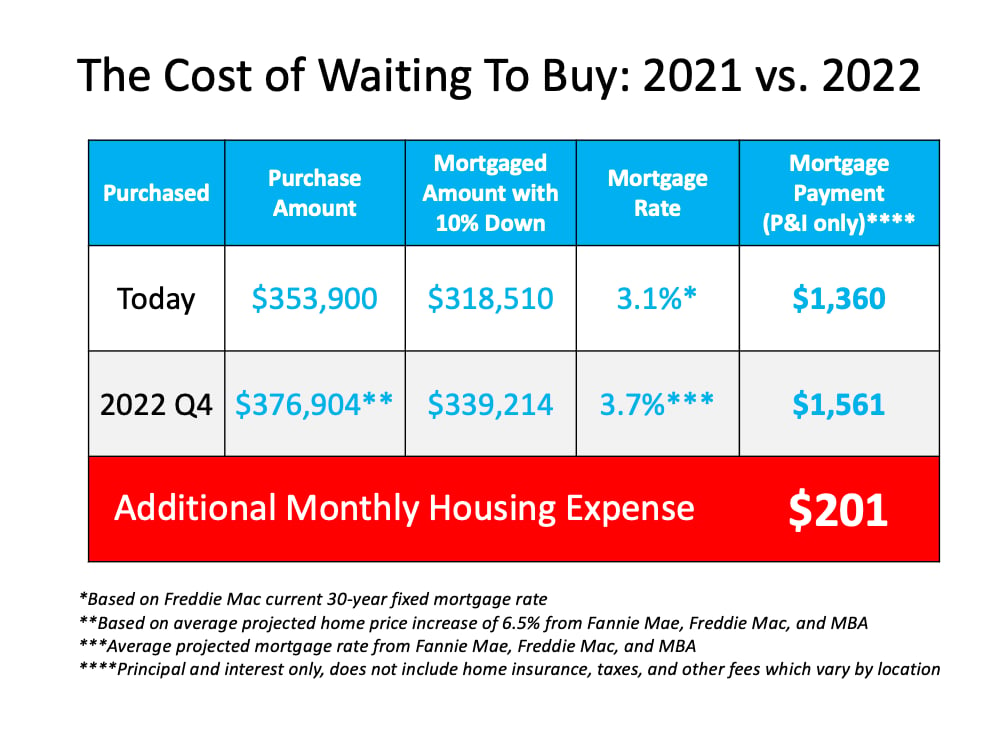

Two Reasons Why Waiting to Buy a Home Will Cost You

Sandy Ginn January 19, 2022

Sandy Ginn January 19, 2022

One simple filing can significantly reduce your Indiana property taxes. Here’s what every homeowner should know about the Homestead Exemption.

From farmers markets and concerts to bike trails and family festivals, discover the best ways to enjoy summer across Greater Indianapolis.

Discover which backyard upgrades buyers value most in 2026 and how the right outdoor improvements can boost both enjoyment and resale potential.

A little preparation now means more relaxing, boating, bonfires, and effortless weekends once lake season arrives.

New buyer data reveals where Steuben County’s luxury lake home purchasers are coming from—and why demand for Indiana lake living remains strong.

A clear, step-by-step look at the inspection process—so first-time buyers know what matters, what to expect, and how to move forward with confidence.

In today’s complex market, having the right representation isn’t just helpful—it’s a strategic advantage that can shape your entire homebuying experience.

Buying your first home isn’t about timing the market—it’s about knowing when your finances, goals, and lifestyle are aligned.

From inspections to financing, here’s what causes deals to fall apart and how buyers and sellers can stay one step ahead.

With experience in every type of real estate transaction, we aim to deliver sound advice, extensive research, and tenacious negotiating in order to secure incredible results for our clients. Every opportunity to serve our clients is a beautiful gift worth cherishing.